Understanding the Importance of Budgeting

Budgeting plays a pivotal role in managing personal finances effectively. It is a structured approach to tracking income and expenses, enabling individuals to allocate their financial resources wisely. By establishing a budget, one gains better control over financial transactions, allowing for more informed and conscious spending decisions. This financial discipline is crucial to overcoming the common pitfalls that many face when managing their finances.

One of the primary benefits of budgeting is the ability to reduce debt. Individuals who monitor their spending are more likely to identify unnecessary expenses that can be trimmed from their budget. This newfound awareness encourages a proactive approach to financial health, ultimately leading to a decrease in reliance on credit cards and loans. By adhering to a budget, individuals can prioritize debt repayment, leading to financial freedom and enhanced credit scores.

In addition to reducing debt, budgeting allows for effective long-term planning. It provides a roadmap for future expenses, whether they are for planned purchases, vacations, or emergencies. With a well-structured budget, individuals can allocate funds towards savings and investments, which are vital for building wealth over time. This foresight can facilitate better preparedness for unforeseen circumstances, such as medical emergencies or unexpected job loss, by ensuring that savings are available to cover such incidents.

Ultimately, the benefits of budgeting extend beyond mere number-crunching. It fosters a mindset of financial accountability and responsibility, encouraging individuals to be more intentional with their money. By understanding and implementing a budget, individuals position themselves on the path towards financial stability, security, and success.

Setting Realistic Budget Goals

Establishing clear and achievable budget goals is essential for effective financial management. The first step in this process is to assess your total income. It is crucial to account for all sources of income, including full-time employment, freelance work, investments, or any side businesses. This comprehensive understanding of your income will provide a foundation upon which to build your budget.

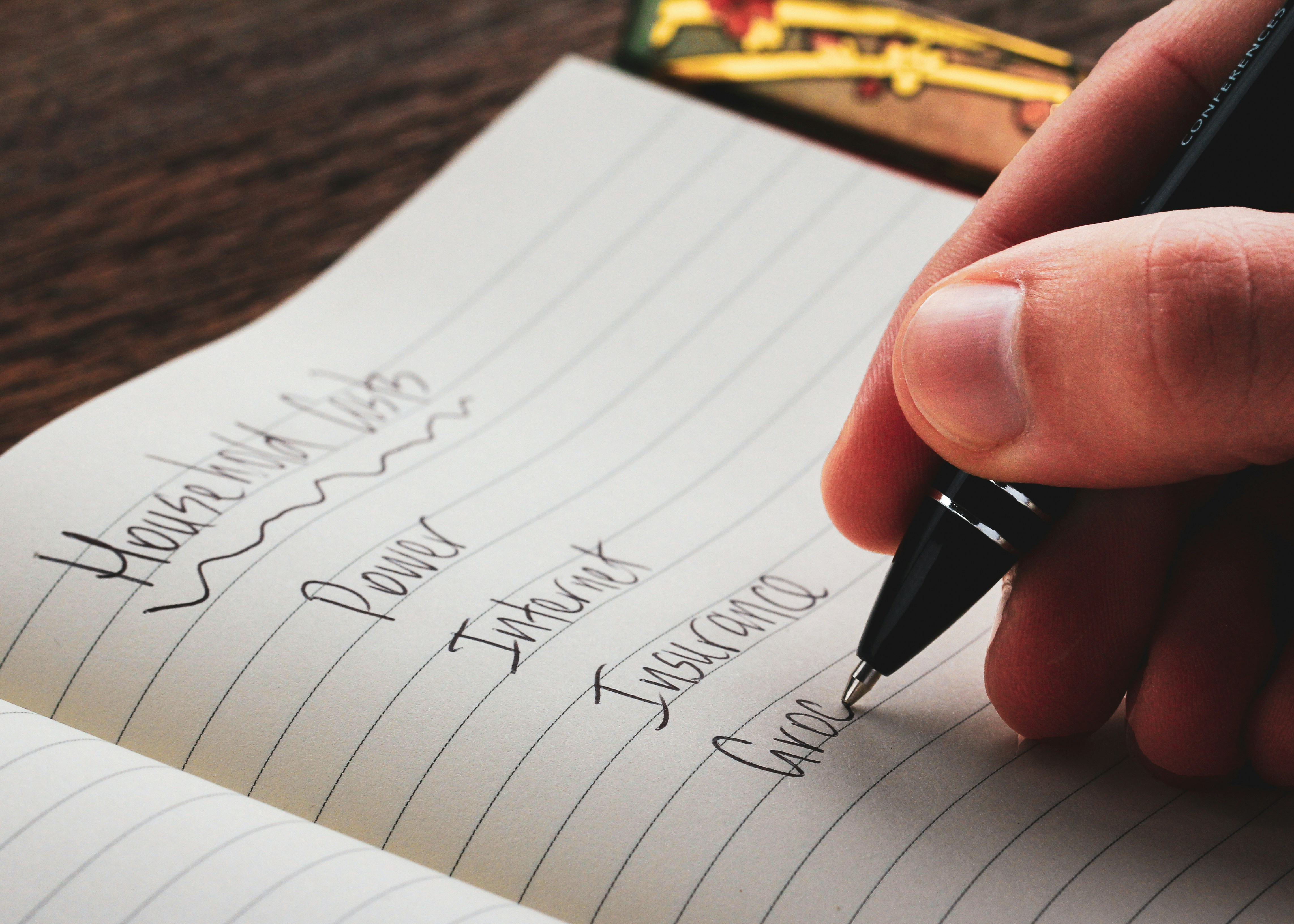

Once your income is clearly assessed, the next step involves understanding the difference between fixed and variable expenses. Fixed expenses are those that remain constant each month, such as rent or mortgage payments, car loans, and insurance premiums. Conversely, variable expenses include fluctuating costs, such as groceries, entertainment, and dining out, which can be adjusted based on your financial situation. By identifying these two categories, you can effectively manage your expenses and allocate funds accordingly.

It is also important to prioritize your financial goals. This can involve short-term objectives, such as saving for a vacation or paying off a credit card, as well as long-term aspirations, including forming an emergency fund, saving for retirement, or purchasing a home. A simple yet effective method for prioritizing these goals is to label them as essential or non-essential. Essential goals typically relate to immediate financial stability, while non-essential ones can be postponed if necessary.

Another useful technique is the S.M.A.R.T. criteria—ensuring that your goals are Specific, Measurable, Achievable, Relevant, and Time-bound. This framework can help refine your budgeting ambitions, making them more attainable by breaking them down into smaller, manageable tasks. As you navigate the financial landscape, remember that setting realistic budget goals is integral to maintaining control over your financial future.

Creating a Personal Budget: Step-by-Step

Creating a personal budget is a fundamental practice for effective financial management. This methodical approach ensures that individuals can effectively track their income and expenses, ultimately assisting in maintaining financial stability. The following steps provide a comprehensive guide for creating a personal budget.

First, begin by gathering all necessary financial documents. This includes pay stubs, bank statements, bills, receipts, and any other relevant financial records. Having accurate and up-to-date information is crucial to establishing a sound budget. Understanding your total income will serve as the foundation for the budgeting process.

Once your financial documents are collected, the next step involves categorizing your expenses. It is advisable to separate expenses into fixed costs, which do not change month to month, such as rent or mortgage, and variable costs, which may fluctuate, like groceries and entertainment. This categorization simplifies the budgeting process and allows for a clearer understanding of where your money is allocated.

Following the categorization, it is essential to set limits for each expense category. This requires analyzing your spending patterns and determining a realistic amount to allocate to each category. Ensure that your total expenses do not exceed your total income. This alignment is critical as it helps to prevent overspending and maintains adherence to the budget.

Regularly reviewing and adjusting your budget is also an important part of this process. Monthly check-ins allow you to track your spending against the established limits, ensuring you stay on course. If certain areas require more or less financing, make necessary adjustments while staying aligned with your financial goals.

In conclusion, following this structured approach to budgeting empowers individuals to take control of their finances, ensuring that they remain within budgetary limits while pursuing their financial aspirations.

Utilizing Budgeting Tools: Tables and Lists

Effective budgeting is crucial for maintaining financial stability and ensuring that expenses do not exceed income. One of the best ways to track your finances is through the use of budgeting tools such as tables and lists. These tools can provide an organized and visual representation of your financial situation, making it easier to manage your budget in a structured manner.

One popular approach to budgeting is the implementation of a spreadsheet. Spreadsheets, such as those created with Microsoft Excel or Google Sheets, allow users to customize their budget according to their unique financial needs. By creating a simple table, individuals can list their income sources alongside their expenses. This method not only provides a clear view of income versus expenses but also allows for easy adjustments as financial circumstances change.

For those who prefer a more ready-to-use solution, numerous budgeting applications are available. Tools like Mint, YNAB (You Need A Budget), and EveryDollar offer user-friendly interfaces that help track spending, categorize expenses, and set saving goals. Many of these apps can sync with bank accounts to provide real-time updates on financial activity, enhancing the effectiveness of personal budgeting. Users can leverage these applications to create visualizations of their spending habits, making it easier to identify areas where cuts can be made.

Moreover, incorporating lists into your budgeting strategy can greatly assist in managing finances. A simple yet effective budgeting list can include categories like fixed expenses (rent, utilities), variable expenses (food, entertainment), and discretionary spending. By regularly updating these lists, individuals can stay accountable and ensure their budget remains within the defined limits.

Incorporating these budgeting tools, whether through tables, spreadsheets, or applications, plays an essential role in personal finance management. They are instrumental in helping users maintain oversight of their financial health, track obligations, and implement actionable insights to adhere to their budget effectively.

Tracking and Monitoring Your Spending

Maintaining a budget requires consistent vigilance regarding your spending habits. Tracking and monitoring your expenses is a foundational step in ensuring that you remain within your financial limits. By regularly reviewing your expenditures, you can identify patterns that could lead to overspending, allowing you to make informed adjustments to your budget.

There are several effective methods for monitoring your spending. One popular approach is to utilize budgeting apps that simplify the process by tracking transactions in real time. These apps often allow users to categorize expenses, set limits for different spending categories, and provide insights into spending habits. Alternatively, a traditional method such as maintaining a handwritten ledger or spreadsheet can offer a more tactile experience for individuals who prefer a manual approach.

Regardless of the method chosen, the key lies in consistency. Make it a habit to check your spending at regular intervals — weekly, bi-weekly, or monthly. This review process will help you understand where your money is going and reveal areas where adjustments are necessary. For instance, if you notice that dining out is consuming a significant portion of your budget, you may decide to reduce those expenses by limiting restaurant visits or opting for more affordable meal options.

Moreover, staying attuned to your spending can help identify unexpected expenses that may arise from time to time. This awareness allows you to set aside a portion of your budget for emergencies or unplanned costs, ensuring that you do not derail your financial goals. By actively tracking and monitoring your spending, you equip yourself with the knowledge needed to adhere to your budget and minimize the risk of overspending.

Recognizing and Addressing Budget Overruns

Identifying when your spending exceeds the budget is crucial for maintaining financial stability. One of the first steps in recognizing budget overruns is to monitor your expenses regularly. Keeping track of every purchase, whether it’s a large expenditure or a small daily item, allows you to see patterns in your spending habits. You may find it useful to utilize budgeting apps or spreadsheets that categorize expenses, enabling you to view where your money goes at a glance.

Another method to pinpoint budget overruns is to compare your actual spending against budgeted amounts on a monthly or weekly basis. This comparison can reveal categories where overspending is evident. For instance, if your budget allocates a certain amount for groceries, yet you consistently exceed this figure, it may be indicative of a need for reevaluation of your grocery shopping habits or budget allocation.

Addressing budget overruns involves taking proactive steps to correct the course. When you notice an overspend, start by analyzing the reasons behind it. Were there unexpected expenses, or was there a deliberate decision to spend more? Understanding the cause of overruns allows you to create strategies to mitigate them in the future. For instance, you might consider setting up an emergency fund for unforeseen costs, or adjusting your budget categories to better reflect your actual spending patterns.

Additionally, it is beneficial to prioritize your needs versus wants. When faced with an overspend situation, evaluate upcoming purchases critically to determine if they are necessary. You may find that delaying certain non-essential purchases can help you stay within budget. By adopting mindful spending habits and adjusting your budget as needed, you can effectively manage and prevent further budget overruns.

The Role of Emergency Funds in Budgeting

In personal finance, an emergency fund plays a crucial role in maintaining financial stability. It serves as a financial safety net during unforeseen circumstances such as medical emergencies, car repairs, or sudden job loss. Without an emergency fund, unexpected expenses can severely disrupt one’s budgeting efforts, forcing individuals to resort to credit cards or loans, which further strain their financial situation.

To establish an effective emergency fund, it is essential to set a realistic target. Financial experts often recommend that individuals aim to save three to six months’ worth of living expenses. This amount can vary based on personal circumstances, such as job security and family size. Individuals should assess their financial situation to determine the right amount that would provide adequate coverage against emergencies.

Building an emergency fund requires discipline and strategic planning. A good starting point is to automate savings by directing a specific percentage of income into a dedicated savings account each month. This approach not only facilitates consistent contributions but also reinforces the habit of saving. Moreover, selecting a high-yield savings account can help grow the funds over time, providing an additional cushion in emergencies.

Maintaining the emergency fund is equally important. It is advisable to avoid using these funds for non-emergency purposes, which can erode the financial buffer built over time. Regularly reviewing and adjusting the emergency fund according to changes in personal circumstances, such as a pay raise or an increase in living expenses, can help ensure that it effectively meets future needs.

By prioritizing an emergency fund within one’s budget, individuals can protect themselves from sudden financial shocks, ensuring that they remain on track with their broader financial goals. This thoughtful approach to budgeting can lead to a more stable and secure financial future.

Adjusting Your Budget for Life Changes

Life is replete with changes, many of which can significantly impact one’s financial situation, necessitating an adjustment of the personal budget. Key events such as a job change, relocation, or the arrival of a new family member can create shifts in income and expenses. Understanding how to effectively modify your budget in response to these changes is crucial to maintaining financial stability.

When one experiences a job change, it often brings fluctuations in income, either increasing or decreasing monthly earnings. Therefore, it is essential to reassess your existing budget. Begin by documenting your new income sources, including any potential bonuses, commissions, or overtime opportunities that may arise in your new position. In tandem, evaluate fixed and variable expenses to accommodate for any anticipated changes in costs associated with your new employment situation, such as commuting expenses or work attire.

Relocation is another significant factor that can affect your budgeting strategy. Moving to a new city or even a different neighborhood can lead to variations in housing costs, utility rates, and local taxes. Adjust your housing budget to reflect these new expenses while potentially allocating funds to cover one-time moving costs. Additionally, assess local amenities and their associated costs, such as groceries or healthcare, which may differ from your previous location.

Additions to the family, such as the birth of a child or a relative coming to live with you, also require a reassessment of financial commitments. A growing family typically brings increased expenses, including childcare costs, education, and healthcare needs. It is advisable to create a separate budget category for these new expenses to accurately track and manage your finances.

In conclusion, life changes necessitate a flexible budgeting approach. Regularly reviewing and adjusting your personal budget in response to job changes, relocations, or family additions can help ensure that your financial plans remain viable and effective, ultimately contributing to your long-term financial health.

Conclusion: Maintaining Financial Discipline

Maintaining financial discipline is crucial for individuals who wish to adhere to their budget and achieve long-term financial stability. A well-structured budget serves as a roadmap, guiding spending habits and financial decisions. However, merely creating a budget is not sufficient; it requires consistent effort and a commitment to follow it diligently.

One key aspect of financial discipline is monitoring expenses regularly. Keeping a detailed record of all expenditures allows individuals to identify spending patterns and make necessary adjustments. Utilizing budgeting tools or apps can facilitate this process by providing real-time insights into financial health. Moreover, reviewing the budget periodically—such as on a monthly or quarterly basis—ensures its relevance, taking into account changes in personal circumstances or financial goals.

Setting realistic and specific financial goals is another essential element. Goals should be SMART: Specific, Measurable, Achievable, Relevant, and Time-bound. This approach helps in motivating individuals to stay committed to their budget. Furthermore, by celebrating small milestones achieved along the way, individuals can foster a positive attitude towards their financial journey.

Another critical factor is understanding the difference between needs and wants. Prioritizing essential expenses over discretionary spending is vital in maintaining budgetary discipline. This requires making conscious decisions and exercising restraint in areas where overspending may be tempting.

Ultimately, financial discipline is not an isolated practice; it is a continuous endeavor. By cultivating healthy financial habits, individuals can sustain their budget over the long term, ensuring they remain on a path toward financial independence. As long as one remains vigilant and adaptable, achieving financial health can become an attainable reality.

Token: Complete 2025 Guide to Decentralized Oracles & Blockchain Integration")

")